Home / Claims Settlement / International agreements / Protection of Visitors

Protection of Visitors

Protection of Visitors

Within the field of international motor vehicle insurance claims settlement, the term “protection of visitors” refers to the protection of individuals who suffer road traffic accidents abroad. The protection of visitors’ system covers accidental damage abroad and should not be confused with the Green Card system, which covers accidental damage at home.

The need for protection arises from the fact that the injured party must rely on a foreign liable driver or his insurer to assert a claim. On the one hand, foreign law is applicable in most cases, on the other hand, language problems may make direct communication difficult or even impossible.

In order to overcome these difficulties, the protection of visitors’ system provides that each country should operate its own information centre to provide information about handling claims abroad. It helps to determine the responsible insurer and provides further information necessary for the processing of a claim. If provided for in the relevant agreements, it locates the competent regulatory body in the State of residence and ensures that injured parties receive their claims within a reasonable time.

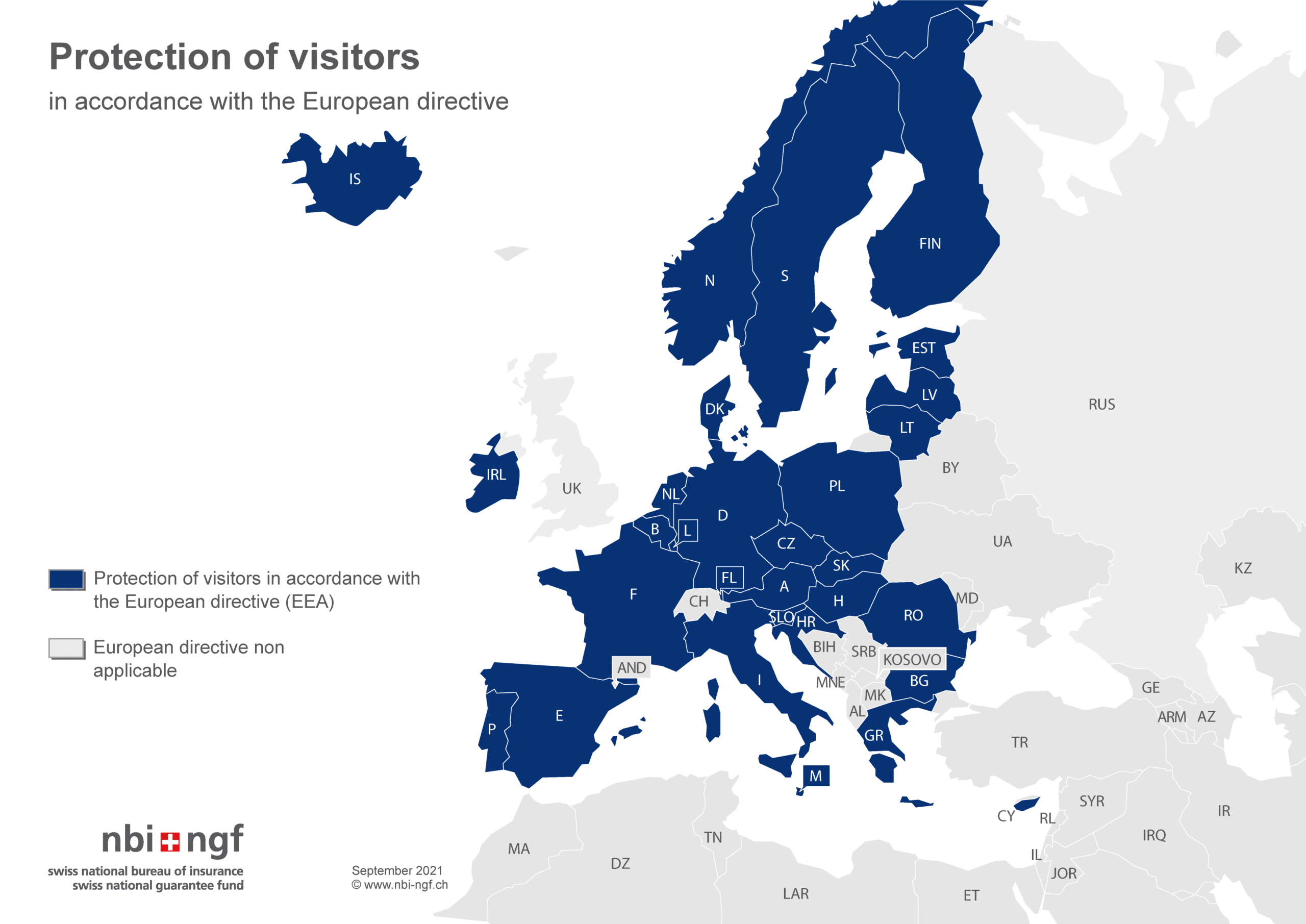

Protection of Visitors in Europe

Please note:

The protection of visitors’ system must be clearly distinguished from the Green Card system. The Green Card system ensures that motorists have sufficient liability insurance cover when travelling abroad. It ensures that injured parties who suffer an accident caused by a foreign vehicle in a country belonging to the Green Card system can file their claims with the national bureau of insurance of that country or with the foreign insurer’s correspondent. In simple terms, the Green Card system protects the injured party in Switzerland against foreign vehicles. In contrast, the protection of visitors’ system protects Swiss injured parties in accidents abroad.

European Directive

Protection of Visitors in accordance with the European Directive

The 4th Motor Insurance Directive (Directive 2000/26/EC) was issued on 16 May 2000. This Directive (the provisions of which were transferred to Directive 2009/103/EC on 16 September 2009) obliges the EEA member states to introduce various provisions on the protection of injured parties who have suffered road traffic accidents abroad.

Claims processing by claims representatives

In accordance with Directive 2009/103/EC (or with the national legislation implementing this Directive), all insurance companies operating within the EEA are obliged to nominate claims representatives (CRs) in each of the other member states.

Victims of an accident abroad can thus file a claim in their country of residence via the CR of the relevant foreign liability insurer. The CR processes the claim according to the law of the country where the accident took place and in accordance with the instructions of the foreign insurer that nominated it.

Information provided by information centres

In order to ensure that injured parties receive the information necessary to pursue their claims and can address themselves to the body responsible for settling their claims, member states have been required to set up information centres. These information centres shall provide injured parties with the address of the competent motor insurers and their claims representatives. Where necessary for the settlement of the claim, information centres shall also inform injured parties of the names and addresses of the owners of the vehicles of the parties responsible for the accident.

Failure protection by the compensation bodies

Directive 2009/103/EC obliges the member states to set up compensation bodies. These bodies provide injured parties with protection against loss or damage in the event of failure to settle the claim properly. If the insurer has not appointed a claims representative or if the representative fails to make an offer of compensation or to provide a reasoned reply to the injured party within a period of three months, the injured party may apply to the compensation body in his state of residence. If the conditions are met, the compensation body shall settle the claim in place of the missing or defaulting claims representative. This also applies if the insurer responsible cannot be identified within two months, either because the person responsible for the accident or his vehicle cannot be identified, or because there is no insurance.

Implementation of the Motor Insurance Directive in Switzerland

The EEA member states were obliged to implement Directive 2000/26/EC by no later than 20 January 2003. Switzerland implemented this Directive independently and integrated the corresponding provisions into Art. 79a of the Swiss Road Traffic Act (SVG) with effect from 1 February 2003.

Applicability to accidents in Switzerland

In the case of accidents occurring in Switzerland, Art. 79a to d SVG apply largely without restriction. Accordingly, the information centre provides injured parties with information on the regulatory body with which they can assert their claims. Swiss motor vehicle liability insurers must respond to the claims of injured parties within three months. Otherwise the compensation body will settle the case.

Applicability in relation to the EEA

In relation to the EEA member states, Art. 79a to d SVG are not applicable. The Directive 2000/26/EC obliges the EEA member states to implement the provisions on the protection of visitors in relation to other member states. Switzerland therefore does not fall within the scope of these provisions.

In order to avoid that Swiss legislation only protects injured parties domiciled in the EEA but not injured parties domiciled in Switzerland (because Directive 2000/26/EC does not oblige insurers domiciled in the EEA to appoint claims representatives in Switzerland), the Swiss legislator has provided in Art. 79e SVG that 79a to d SVG are only applicable vis-à-vis another state if the state in question grants Switzerland reciprocal rights. Currently, only Liechtenstein grants Switzerland such a reciprocal right.

In order to guarantee the protection of visitors in relations with the EEA states despite these legal obstacles, the NBI concluded bilateral agreements under private law with its partner associations in the EEA, based on the competence to which it is entitled under Art. 76b para. 5 lit. b SVG.

Implementation of the Motor Insurance Directive in Liechtenstein

In its capacity as a member of the EEA, Liechtenstein was also obliged to incorporate the provisions of Directive 2000/26/EC into its national law. There is full reciprocity between Liechtenstein and the other EEA states in the area of the protection of visitors.

Bilateral Agreements

Protection of Visitors for Swiss injured parties abroad and for foreign injured parties in Switzerland

Switzerland does not fall within the scope of Directive 2000/26/EC. In order to enable road accident victims to benefit from the most important provisions for the protection of visitors, the NBI concluded bilateral agreements under private law with all the competent institutions of the EEA member states based on the competence to which it is entitled under Art. 76b para. 5 lit. b SVG.

The agreements are based on the provisions of Directive 2000/26/EC. Agreements with exchange of information (map above: states coloured light blue) provide that the information centres of the contracting states provide the persons concerned with the necessary information to enable them to assert their claims. Agreements with claims settlement in the state of residence (map above: states coloured dark blue) also require the appointment of claims representatives in the other contracting state to receive claims from injured parties. However, access to compensation bodies is expressly excluded in all bilateral agreements on the protection of visitors.

Agreements on the Protection of Visitors

with exchange of information

The visitor protection agreements with exchange of information provide that injured parties after traffic accidents receive assistance from the information centres in identifying the competent motor vehicle liability insurers and further information. The aim is to ensure that claims are settled in favour of the injured party as quickly and easily as possible. The procedure is initiated by an injured party’s request for information to the insurance bureau of his place of residence. On receipt of the request, the insurance bureau shall contact either the insurance bureau on whose territory the vehicle causing the accident was registered or the insurance bureau on whose territory the accident took place, in order to obtain the following information for the attention of the injured party:

- Identification of the liability insurer of the vehicle involved in the accident

- Identification of the driver, owner or keeper of the vehicle involved in the accident, if the insurer cannot be identified within 6 weeks after the accident

and in addition, depending on the agreement:

- Police report

- Information on any payments from a guarantee fund or other information that may be useful for the settlement of claims

The NBI has concluded agreements on the protection of visitors with exchange of information with the insurance bureaux of the following states:

In force since:

09.05.2014

Morroco, Turkey, Ukraine

01.01.2016

Bosnia and Herzegovina, Macedonia, Moldova, Montenegro, Serbia, Tunisia, Belarus

01.07.2016

Andorra

with exchange of information and claims handling in the state of residence

Haben die Versicherungsbüros zweier Staaten ein Besucherschutz-Abkommen mit Schadenregulierung im Wohnsitzstaat unterzeichnet, sind die Versicherungsgesellschaften dieser Staaten befugt, im jeweiligen anderen Staat Schadenregulierungsbeauftragte zu ernennen. Diese Schadenregulierungsbeauftragten sind unter den folgenden Voraussetzungen zuständig, um Forderungen von Geschädigten zu regulieren:

- Geschädigte haben ihren Wohnsitz im selben Staat wie der Schadenregulierungsbeauftragte.

- Der Unfall hat sich entweder in dem Staat ereignet, in dem der zuständige Versicherer seinen Sitz hat, oder in einem anderen Staat des Grüne Karte-Systems, sofern dieser Staat nicht gleichzeitig Wohnsitzstaat der Geschädigten ist.

Die Schadenregulierung erfolgt nach Massgabe des anwendbaren Rechts. Voraussetzungslose Anerkennungen oder endgültige Abwicklungen bedürfen des Einverständnisses des zuständigen Versicherers. Der Versicherer kann den Schadenfall dem durch ihn ernannten Schadenregulierungsbeauftragten jederzeit wieder entziehen. Er darf dieses Recht jedoch nicht dazu missbrauchen, um berechtigte Ansprüche der Geschädigten zu kürzen. Wo kein Schadenregulierungsbeauftragter ernannt wurde, kann diese Rolle mit dem Einverständnis des zuständigen Versicherers durch das Versicherungsbüro des Wohnsitzstaates der Geschädigten wahrgenommen werden. Der Versicherer kann den Schadenfall auch dem Versicherungsbüro jederzeit wieder entziehen. Die Abkommen sehen weder eine Sanktionierung des Versicherers noch des Schadenregulierungsbeauftragten vor, wenn den Geschädigten keine begründete Antwort auf eine geltend gemachte Forderung erteilt wurde. Die Abkommen sehen auch keine Pflicht zur Zahlung von Verzugszinsen oder Möglichkeiten für einen Fallentzug bei Versäumnissen vor. Sie führen jedoch eine Meldepflicht der Versicherungsbüros untereinander für diejenigen Fälle ein, in denen die Schadenregulierung nicht ordentlich abläuft.

Das NVB hat Besucherschutz-Abkommen mit Schadenregulierung im Wohnsitzstaat mit den Versicherungsbüros der folgenden EWR-Staaten abgeschlossen:

In Kraft seit:

01.10.2003

Österreich, Deutschland

01.01.2004

Belgien, Spanien, Niederlande

01.05.2004

Tschechien, Estland, Ungarn, Polen, Slowakei

15.10.2004

Griechenland

01.01.2005

Frankreich

01.01.2006

Grossbritannien

30.03.2007

Malta

17.08.2007

Rumänien

25.09.2007

Zypern

01.01.2010

Italien

01.09.2016

Bulgarien, Dänemark, Finnland, Irland, Island, Kroatien, Lettland, Litauen, Luxemburg, Norwegen, Portugal, Schweden, Slowenien